12 Critical Mistakes First-Time Home Buyers Make - Expert Guide to Avoid Them

Your home holds a lot of financial potential that could be put to work for your future. Discover how much equity you could tap into with NerdWallet.

First-time home buyers often face challenges navigating today's housing market. Here are 12 common mistakes to avoid during your home-buying journey.

Not calculating affordability first can waste time looking at houses outside your budget. Use a mortgage affordability calculator to determine your comfortable price range before house hunting.

Skipping mortgage preapproval weakens your position as a buyer. Get preapproved before serious house hunting to demonstrate your ability to follow through on offers.

Only getting one mortgage quote could cost you significantly. Compare multiple lenders - borrowers typically save $100+ monthly by shopping rates. Multiple applications within 45 days count as one credit inquiry.

Blue-roofed residential house

Check credit reports for errors before applying. Lenders scrutinize these reports closely, and mistakes could result in higher interest rates. Request free annual reports from all three bureaus.

While 20% down isn't required, saving more reduces monthly payments and often qualifies you for better rates. First-time buyers typically put down 8%. Consider loan programs allowing lower down payments if needed.

Research first-time buyer programs in your state offering grants or favorable terms. Many employers and organizations also provide assistance programs - investigate all options.

Woman holding keychain

Government-backed loans offer advantages:

- VA loans: 0% down for military service members

- USDA loans: 0% down for rural properties

- FHA loans: Down payments as low as 3.5%

Consider mortgage points carefully. Calculate the break-even period to determine if paying points upfront makes sense for your situation.

Maintain adequate savings beyond the down payment for:

- Closing costs

- Moving expenses

- Emergency repairs

- Insurance deductibles

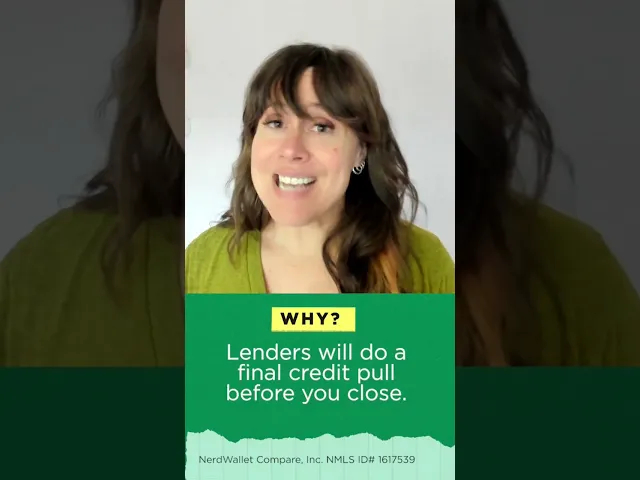

Avoid credit changes between mortgage application and closing. New credit applications or increased debt can affect your loan terms or approval.

Woman with long brown hair

Plan for ongoing homeownership costs:

- Property taxes

- Insurance

- Utilities

- HOA fees

- Maintenance

Get multiple contractor estimates for repairs/renovations. TV shows often underestimate real-world costs and timelines. Work with trusted professionals recommended by both your agent and independent sources.

Related Articles

HELOC Calculator: Compare Home Equity Line of Credit Rates & Payments